[ad_1]

BirdShutterB/iStock via Getty Images

Investment Thesis

General Motors (NYSE:GM) is proof of why the auto industry cannot ignore the legacy ICE segment, also known as, Dinosaurs, despite the recent popularity of pure-play EV players, such as Rivian (RIVN), NIO (NIO), and most notably Tesla (TSLA).

With nearly 6.3M of auto deliveries in FY2021, GM remains a force to be reckoned with for the next two decades, since the ICE market will likely still account for the majority of auto sales in the market then. In addition, with the guidance that “more than half of GM’s factories in China and North America will be capable of EV production” by 2030, we may see the company succeed in its slow but sure transition as a “platform innovator,” with over 3M in EV deliveries by the end of the decade. Furthermore, GM has obtained the enviable “first and only company to operate a commercial, driverless ride-hail service” in San Francisco, much earlier than the supposed global leader in the autonomous vehicle, TSLA, by two years.

Nonetheless, with TSLA guiding for 20M in EV deliveries by 2030, GM may potentially be left behind to play catch up to the EV leader, yet again. In addition, with a market cap of $47.2B, GM still has a long way to go before competing with TSLA at $724.64B. Furthermore, there is a reason why TSLA was awarded the premium, given its leading AI applications, autonomous dreams, and the lofty Optimus robot project. We shall see.

GM Is Still Highly In Demand For Its ICE Segment

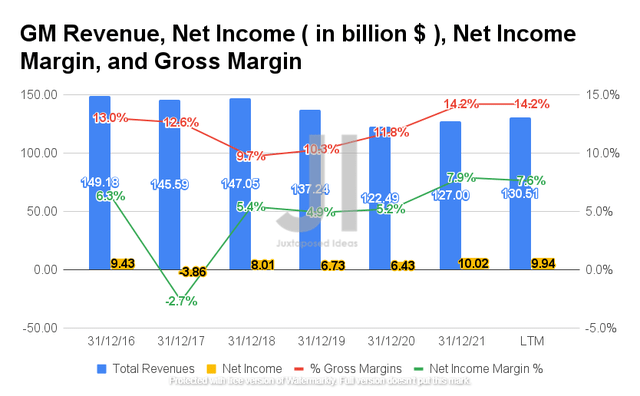

GM Revenue, Net Income, Net Income Margin, and Gross Margin

GM Revenue, Net Income, Net Income Margin, and Gross Margin (S&P Capital IQ)

Given the supply chain issues during the COVID-19 pandemic, it is evident that GM’s sales have been lackluster in the past two years. Nonetheless, the company has been reporting excellent recovery thus far, with improved margins as well. By the LTM, GM reported revenues of $130.51B with gross margins of 14.2%, representing a minimal decline of -4.9% and a massive increase of 3.9 percentage points from FY2019 levels. In addition, the company reported net incomes of $9.94B and net income margins of $7.6B, representing an increase of 47.6% and 2.6 percentage points from FY2019 levels.

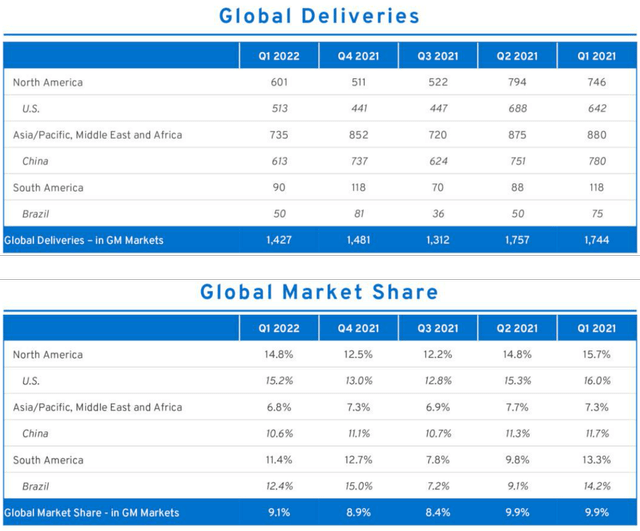

GM’s Strong Auto Delivery and Market Share

GM’s Strong Auto Delivery and Market Share (Seeking Alpha)

As seen from its auto-deliveries of 5.97M in the LTM and its growing market share of 9.1% in the LTM, we can see that GM has performed decently well thus far. Moving forward, we expect the company to successfully erode TSLA’s leading market share in the US from 70% today to potentially 11% by 2025, with both GM and Ford (F) potentially reporting a robust market share of 15% each then.

Given the competitive release of “135 new electric vehicles” by other automakers, including the EV versions of popular models such as Ford’s F-150 and GM’s Hummer, we do not expect GM to lose out as well, with another 17 EV models in its pipeline through 2026. In the meantime, TSLA has continued to push back the production of its Cybertruck, Hatchback, and Roadster for the past two years, with the new proposed timeline in 2023. As a result, we concur with consensus estimates on GM’s projected growth potential indeed.

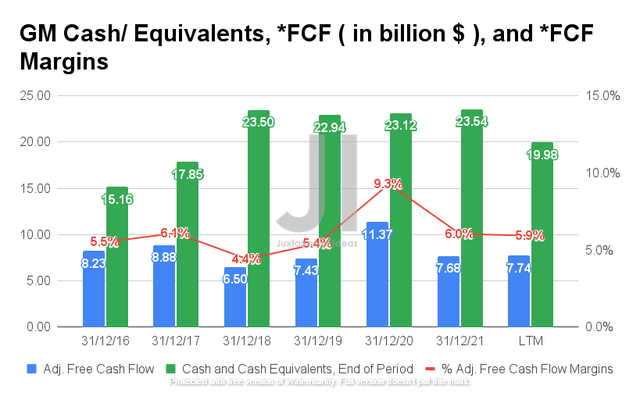

GM Cash/ Equivalents, FCF, and FCF Margins

GM Cash/ Equivalents, FCF, and FCF Margins (S&P Capital IQ)

In the chart above, we have adjusted GM’s Free Cash Flow (FCF) generation accordingly, due to its deceptively high GAAP capital expenditure, comprised of expenditures for property (also known as production capacity ) and purchases of leased vehicles, net (buying back its rental fleet ). As a result, the company reported an adj. FCF of $7.74B and an adj. FCF margin of 5.9% in the LTM, with decent cash and equivalents of $19.98B on its balance sheet. Given that GM guided adj. FCF of up to $9B for FY2022, GM has more than sufficient capital for its expansion in the short and intermediate-term, further boosted by its robust adj. FCF generation.

However, given GM’s estimated $35B in additional spending through 2025 for the expansion of its EVs manufacturing capacity, we reckon that its NTM Market Cap/ FCF multiples and NTM Levered FCF yield would likely fall in the next few years. Thereby, further impacting its stock performance in the intermediate term. Nonetheless, since these would eventually be top and bottom line accretive, we expect GM to perform well in the booming EV market then, which is expected to more than double to $567B by 2025, at a CAGR of 24.37%. Meanwhile, we expect its ICE segment to keep delivering robust sales as well, since it would take the EV’s global sales another two decades to overtake the ICE’s market.

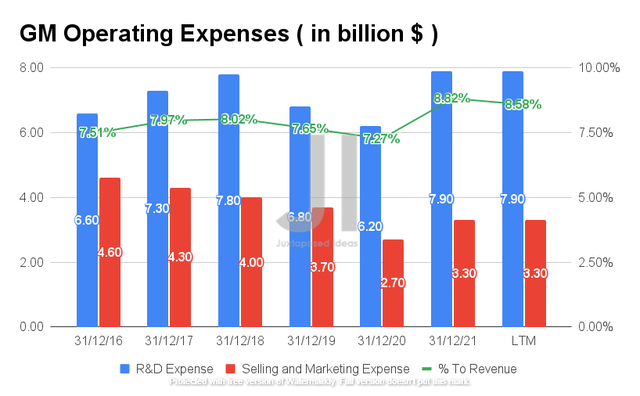

GM Operating Expense

GM Operating Expense (S&P Capital IQ)

In the meantime, GM also reported increased operating expenses in the past year, with a total of $11.2B of R&D and Selling/ Marketing expenses in the LTM. As a result, the company reports a higher ratio in comparison to its reduced revenue at 8.58% in the LTM, compared to 7.65% in FY2019. Nonetheless, we are not overly concerned, given the projected growth in its revenue for FY2022.

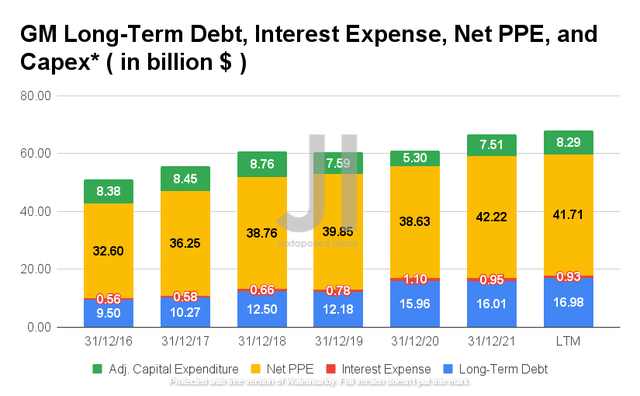

GM Long-Term Debt, Interest Expense, Net PPE, and Capex

GM Long-Term Debt, Interest Expense, Net PPE, and Capex (S&P Capital IQ)

GM has been increasing its reliance on long-term debts over time, which relatively worsened during the COVID-19 pandemic. The company reported long-term debts of $16.98B and interest expenses of $0.93B, representing a notable increase of 39.4% and 19.2% from FY2019 levels. In addition, given the robust consumer demand, GM has also been increasing its net PPE assets and capital expenditure in FY2021, with a total of net PPE assets of $41.71B and adj. Capex (minus auto leasing ) of $8.29B in the LTM. From FY2022 onwards, the company expects to spend up to $10B on Capex, a reasonable investment given its end goal of producing 1M EVs by mid-decade.

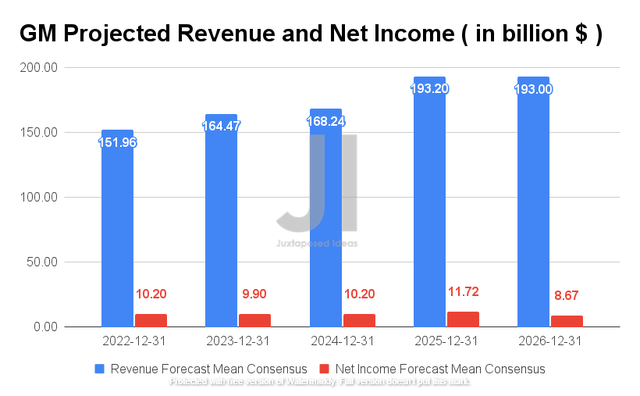

GM Projected Revenue and Net Income

GM Projected Revenue and Net Income (S&P Capital IQ)

Over the next five years, GM is projected to report revenue growth at a CAGR of 11.18%, though its net income profitability is expected to remain broadly in line through FY2025, before normalizing to pre-pandemic levels by FY2026. However, it is also evident that its net income margins are expected to normalize over time, from 4.9% in FY2019, 6.7% in FY2022, and 4.4% in FY2026.

For FY2022, consensus estimates that GM will report revenues of $151.96B and net incomes of $10.2B, representing a remarkable increase of 33.7% and 1.8% YoY. Assuming that GM is able to ship all of its completed vehicles with the required chips, we may also expect to see an upwards rerating of its net income for up to $11.2B. Thereby, boosting its chances for stock recovery by February 2023.

In the meantime, analysts will be looking closely at GM’s FQ2’22 performance, with consensus revenue estimates of $35.21B and adj. EPS of $1.48, representing YoY growth of 3.04% though -24.83% decline, respectively. Nonetheless, given that the supply chain issue is an industry-wide problem, similarly affecting Tesla’s ramping up efforts in Berlin and Texas, we expect further sideways price action instead of a drastic decline post-FQ2’22 earnings call. We shall see.

In the meantime, we encourage you to read our previous article on TSLA, which would help you better understand its position and market opportunities.

- Tesla: Tragic Correction Could Be Coming

- Tesla’s Cinderella-Like Q1 Numbers May Not Survive COVID

So, Is GM Stock A Buy, Sell, or Hold?

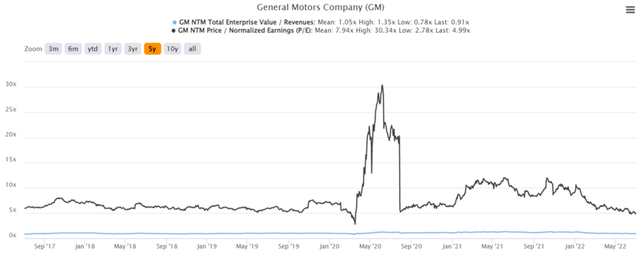

GM 5Y EV/Revenue and P/E Valuations

GM 5Y EV/Revenue and P/E Valuations (S&P Capital IQ)

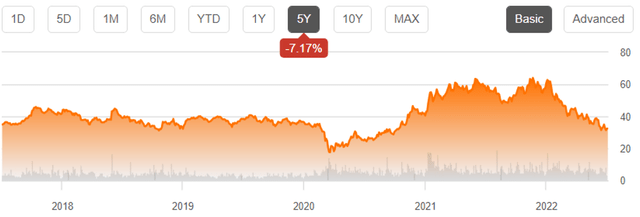

GM is currently trading at an EV/NTM Revenue of 0.91x and NTM P/E of 4.99x, lower than its 5Y mean of 1.05x and 7.49x, respectively. The stock is also trading at $32.37, down 51.8% from its 52 weeks high of $67.21, nearing its 52 weeks low of $30.33. Given the supply chain disruptions in FQ2’22, the GM stock recovery seems far-fetched over the next few weeks, prior to its earnings call in early August 2022.

GM 5Y Stock Price

GM 5Y Stock Price (S&P Capital IQ)

Therefore, despite the attractive buy rating from consensus estimates with a price target of $53.17, we are unconvinced of GM’s 64.26% upside. As a result of the macro issues affecting semi-conductor supply, its projected lower FCF profitability, and its future reliance on long-term debts, GM stock is likely to continue underperforming for a while longer.

Given the potential recession and the Fed’s hike in interest rates, we may also expect to see the market decline further, with the S&P 500 Index already falling 21.8% in the first half of 2022. Though speculative and barring recovery upon a positive catalyst, we could potentially see GM falling to $25 to $28 in the intermediate-term, which would be a comfortable entry point for nibbling.

In the meantime, we rate GM stock as a hold for now.

[ad_2]

Source link